HOME >> BUSINESS

Concern raised over Internet finance

By Wang Xinyuan in Boao Source:Global Times Published: 2014-4-9 23:53:01

The Yu'ebao app, shown on a smartphone Photo: IC

Internet finance weakens the efficacy of monetary policy and poses a challenge to current financial regulations, a bank executive said at a session of the Boao Forum for Asia on Wednesday.

"Internet finance - covering virtual currency and Internet-based financial products - increases market liquidity and speeds up payment, reducing the need for money supply," said Ma Weihua, chairman of Wing Lung Bank.

Ma was also a former head of China Merchants Bank (CMB) and a former central bank official before he joined CMB in 1999.

"Virtual Internet currencies (such as Bitcoin) make it difficult for the central bank to control the overall money supply," Ma noted.

Uncertainty about Internet security is also a significant challenge for financial security, he said.

"You cannot imagine what a tragedy it would be if the Internet were to collapse in a hacker's attack, because all customers' information is on the Web (in the case of Internet finance products)," he said.

The key challenge for regulators is how to ensure Internet security. To protect Internet security is to protect information security, as well as the interests of consumers, he noted.

Ma suggested that regulators take a flexible approach to different areas of Internet finance, rather than creating overall rules for the whole sector, giving it space to grow while preventing financial risks.

Internet-based financial products range from peer-to-peer (P2P) lending to wealth management products and online insurance products.

Internet finance drives innovation in the financial sector, as it enables people to get better services while spending less money, Wang Yincheng, vice chairman and president of the People's Insurance Company (Group) of China Ltd, told the Global Times on Wednesday.

Internet finance has grown quickly in China in recent years, partly because it offers lower financing costs for borrowers and higher investment returns for lenders, Gregory Gibb, chairman of Shanghai Lujiazui International Financial Asset Exchange (Lufax), said at the same forum session.

Ping An Insurance-backed Lufax is a P2P lending platform that generates average annualized returns of 8.6 percent for individual investors, compared with 3 percent from a one-year bank deposit, Gibb said.

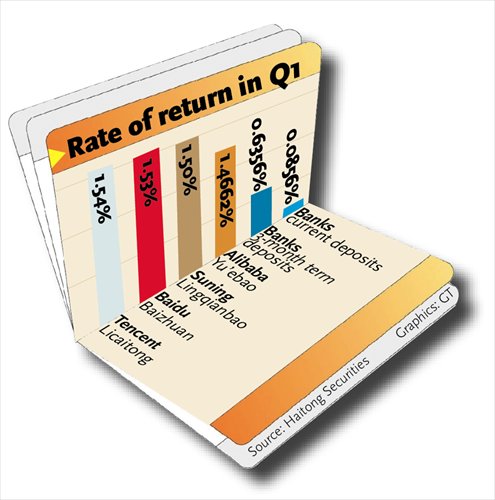

Other types of Internet finance, such as online wealth management products like Alibaba's Yu'ebao and Tencent's WeChat-based Licaitong, have also gained popularity by offering individual investors higher yields than the government-set bank deposit rate, which has not yet been fully liberalized.

The rapid growth of Internet finance has become a problem for State-controlled banks, which are finding it more difficult to attract bank deposits now that people are being tempted by higher returns from online products.

The People's Bank of China, the central bank, recently tightened regulations by suspending the launch of virtual credit cards and mobile payment via QR codes. The central bank said it was intended to protect consumers' financial security, but the move was seen by many as an effort to support banks by reining in the development of Internet finance.

A minimum requirement or entry threshold should be imposed on Internet finance providers, Chen Long, a finance professor at the Cheung Kong Graduate School of Business, told the Global Times on Wednesday on the sidelines of the forum.

The central bank is also reportedly mulling draft rules that would cap single transfers through individual third-party payment accounts at 1,000 yuan ($161), with a cap on cumulative transfers of 10,000 yuan a year.

"That would kill Internet finance," Chen said.

There will be moderate supervision of Internet finance, which will require coordination among different government agencies, Yan Qingmin, vice chairman of the China Banking Regulatory Commission, said at a session of the forum on Tuesday.

Read more in Special Coverage:

Posted in: Industries