COMMENTS / EXPERT ASSESSMENT

China steps up digital currency rollout, deepens cooperation with SWIFT

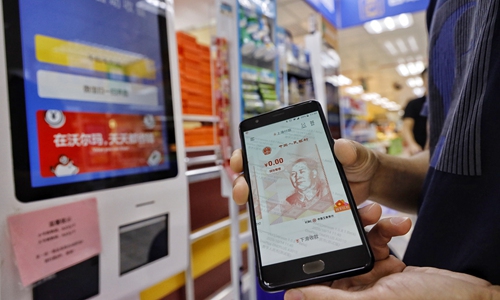

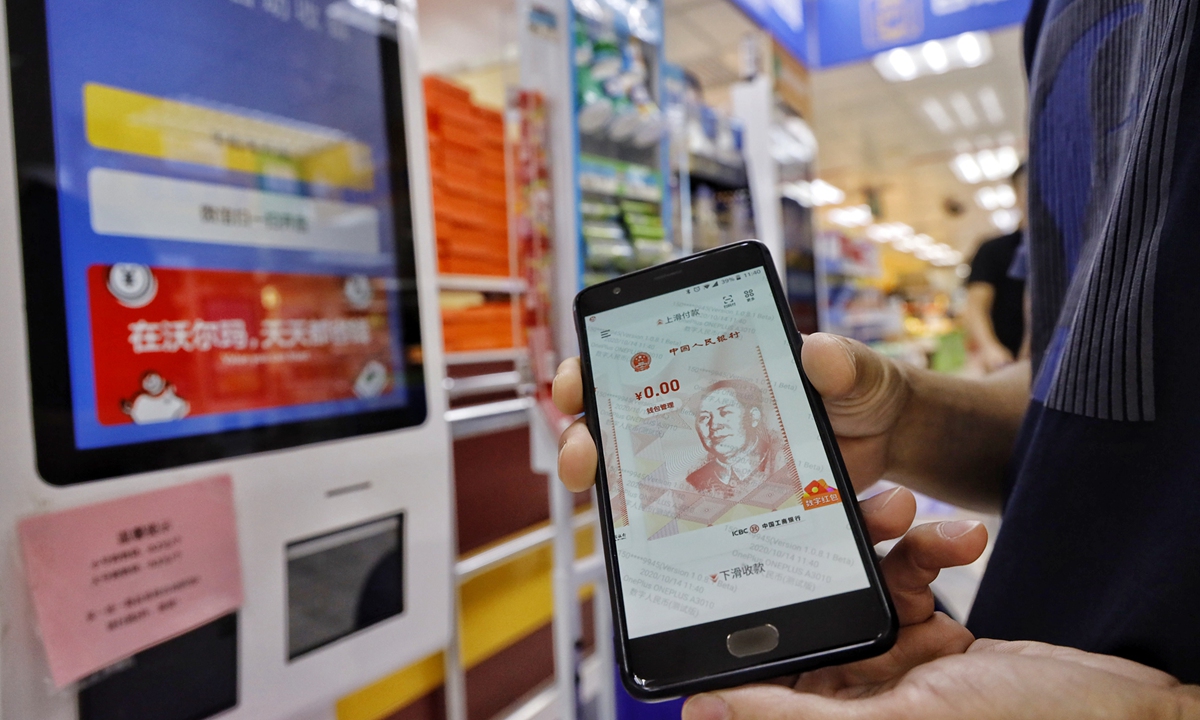

Residents who received "red packets" of digital RMB use the money in stores in Shenzhen, Guangdong Province, on Wednesday. The city launched a pilot program to distribute 10m yuan ($1.49m) in the form of digital currency to residents on Monday. Photo: Li Hao/GT

During the Chinese Lunar New Year holiday, a new round of trials for Digital Currency/Electronic Payment (DCEP) developed by the People's Bank of China (PBC) continued to be rolled out across selected Chinese cities - Beijing, Suzhou and Shenzhen, distributing millions of dollars to local consumers while testing many new features.

The rise of digital currencies is likely to be a gamechanger for the global currency system. As more countries' central banks begin engaging in research and development competition, China leads the way.

In 2019, the PBC, China's central bank, had basically completed the top-level design, standard formulation, function research and development, and joint debugging and testing of DCEP. China has launched tests of DCEP in several cities since April 2020.

The technology design and operation framework of the digital currency is now almost complete. Major commercial banks have made preparation in technology, system building and operation management for the rollout of the DCEP. The rollout of the DCEP in China is now just on the horizon.

As a rising digital superpower, China is entering a fully mobile internet era, with China's online population surging to almost 1 billion. A massive user population and vast mobile apps have set solid foundation for the application of digital currency. In contrast with other countries, China enjoys great advantage in promoting digital currency.

Based on specific designs, DCEP can realize transfer and point-to-point exchange with only digital wallets rather than bank accounts. While satisfying the current payment needs of online banks, WeChat Pay under Tencent and Alipay under Alibaba, the DCEP can also break the defects of these payment modes' reliance on internet. As the PBC continues expanding trials sites, the implementation and promotion of the DCEP across the country will step up.

SWIFT, the global system for financial messaging and cross-border payments, on January 16 set up a joint venture - Finance Gateway Information Services Co - with the Chinese central bank's digital currency research institute and clearing center. After officially establishing a wholly-owned entity in Beijing in June 2019, the new strategic move of SWIFT marks its deepening cooperation with China.

On the one hand, this move is of positive significance for SWIFT to promote internal reform and technological innovation. Facing the challenge of the oncoming digital currency era, SWIFT must be prepared for the future in terms of system and technology. China's leading position in the global competition of digital currency will provide a very important sample and reference for SWIFT to cope with the new challenge of digital currency reform.

On the other hand, to realize cross-border payment and flow in the future, the DCEP will face complex problems compared to its domestic use. This will depend on extensive, in-depth and close international cooperation and research.

The joint venture established by the PBC, especially its digital currency research institute, and SWIFT is not only of great significance to both sides' in-depth exploration of solutions to cross-border payment and flow of global digital currency, but also is expected to explore a feasible mode and technical path for DCEP to go abroad.

In addition, from the perspective of the renminbi's internationalization, the cooperation between China and SWIFT will further promote the improvement of renminbi cross-border payment infrastructure and expand the network system of renminbi cross-border payments. SWIFT is a global financial messaging service platform established by international banks to unify the channel, standard and language of fund payment and settlement. It operates a global financial message network, connects with more than 11,000 banks, financial institutions, financial market infrastructure and enterprise users, and covers more than 200 countries and regions.

The author is Senior Executive Vice President of Bank of China Johannesburg Branch. bizopinion@globaltimes.com.cn

RELATED ARTICLES