Illustration: Liu Rui/GT

India has overtaken UK to become the world's fifth-largest economy, according to the latest calculations by Bloomberg. The piece of news is set to serve as a bitter reminder to UK's incoming prime minister of the bleak economic outlook facing the country, which is in urgent need of being pragmatic and courageous to resolve the real problems perplexing UK.According to the GDP figures from the IMF, India already overtook UK in the final three months of 2021, and its lead over the UK widened in the first quarter this year. On an adjusted basis and calculated in US dollars, the size of the Indian economy reached $854.7 billion in the first three months of this year, while that of the UK was only $816 billion. The IMF projected that India would overtake UK on an annual basis in 2022.

For a long time, there have been no short of Indian media reports accusing UK of pointing a finger at India's foreign policy and domestic issues with a kind of colonial arrogance. Now as a former British colony, India's leap over the UK in economic size could be seen as a development of historical significance, as well as a blow to those who are still addicted to the memories and colonial dreams of the past glory.

Objectively speaking, there exists certain inevitability for India to surpass UK in economic size. With its massive demographic dividend, India is currently the fastest growing major economy in the world, with GDP expanding 13.5 per cent in the April-June quarter, the quickest pace in many years.

By comparison, UK is facing the growing risks of a recession that the Bank of England says may last well into 2024. Against this backdrop, the catch-up and overtaking between the two vastly different economies is a sure thing.

But the timing of the news is delicate. UK Conservative Party members are set to choose the new prime minister on Monday, who will oversee a nation facing the highest levels of inflation in four decades and a myriad of societal problems arising from the economic decline. There is no doubt the incoming UK prime minister's top priority is to deal with the problems such as soaring energy prices and cost of living.

Inflation in the UK rose above 10 percent for the first time in four decades in July, and Goldman Sachs recently warned that the figure could top 22 percent next year, close to the post-war record set in 1975.

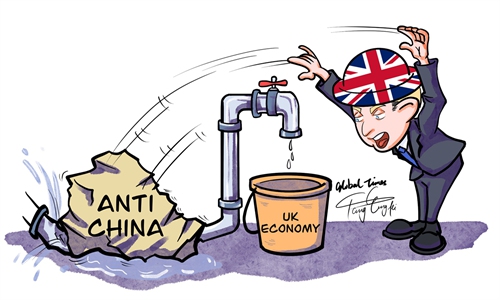

It should be noted that the economic problems facing Britain today are due in large part to its geopolitical misjudgment that London has politicized normal economic and trade cooperation.

Following the reckless and disastrous Brexit, UK has always followed the US in making waves on the geopolitical arena. If anything, the surging inflation in the UK is partly caused by its joining US-led sanctions against Russia, which has led to a jump in energy prices.

What's more ridiculous is that UK's prime minister candidates have competed on their inflammatory rhetoric toward China, a major trade and economic partner for many years. At a time when UK politicians' attitude toward China is increasingly tough and irrational, the country's economic problems including inflation, soaring cost of living and risks of a recession is to become more serious.

What UK needs now is to look itself squarely in the mirror, abandon mindset of playing geopolitical gambit by always following the steps of Washington. There is no good in continuing to play geopolitical gimmicks. London could try to turn to India, China and other emerging market economies to seek more opportunities.

The world's economic gravity has been moving steadily eastward, and the Asian Century is coming. UK needs to jump on the Asian bandwagon and consider how to better cooperate with Asian economies, so that it won't be left far behind by India.

RELATED ARTICLES