Illustration: Chen Xia/Global Times

Some Western media outlets have showed signs of blaming China for the inflation problems facing the global economy, but it only reflects their anxiety and lack of confidence in the West's ability to clean up their own mess, which is a typical manifestation of self-delusion.The latest example is a Bloomberg article on Thursday entitled "China Is the Wild Card for Global Inflation in 2023," which stated that inflation around the world is expected to slow next year, but China's economic rebound could rattle those expectations by putting upward pressure on global prices.

These days, some in the West seem particularly adept at finding "fault" with the Chinese economy. According to these critics, an economic slowdown could be a drag on global economic growth, while a recovering Chinese economy may become an inflationary force for the global economy. But such biased arguments are untenable and even with malicious intentions.

At present, the global economy faces growing recession risks due to geopolitical tensions, high inflation, supply chain crisis and other factors. Anyone who has the basic knowledge about the situation would know that China remains a positive force for global prosperity and development. This is because China's long-term economic fundamentals remain sound and the continued momentum of economic recovery has not changed.

Moreover, the Chinese government has announced a series of measures to further optimize COVID-19 response and to stabilize the economy, sending a strong signal of boosting economic growth and promoting consumption, which have further strengthened the market confidence in the Chinese economy.

Despite some degree of short-term impact, the disruption of the epidemic on economic activities in China will gradually weaken in the long run, and the economy will return to normal operation on the whole. For instance, a report from Goldman Sachs said that China's GDP growth is likely to pick up in the second half of 2023 and continue the trend in 2024. Optimism has already been felt in the international and domestic capital markets over the past week.

It should be noted that while the continuous optimization of China's epidemic control and prevention measures are expected to boost consumption, there is no reason for the West to pass the buck to China when it comes to tackling unchecked inflation.

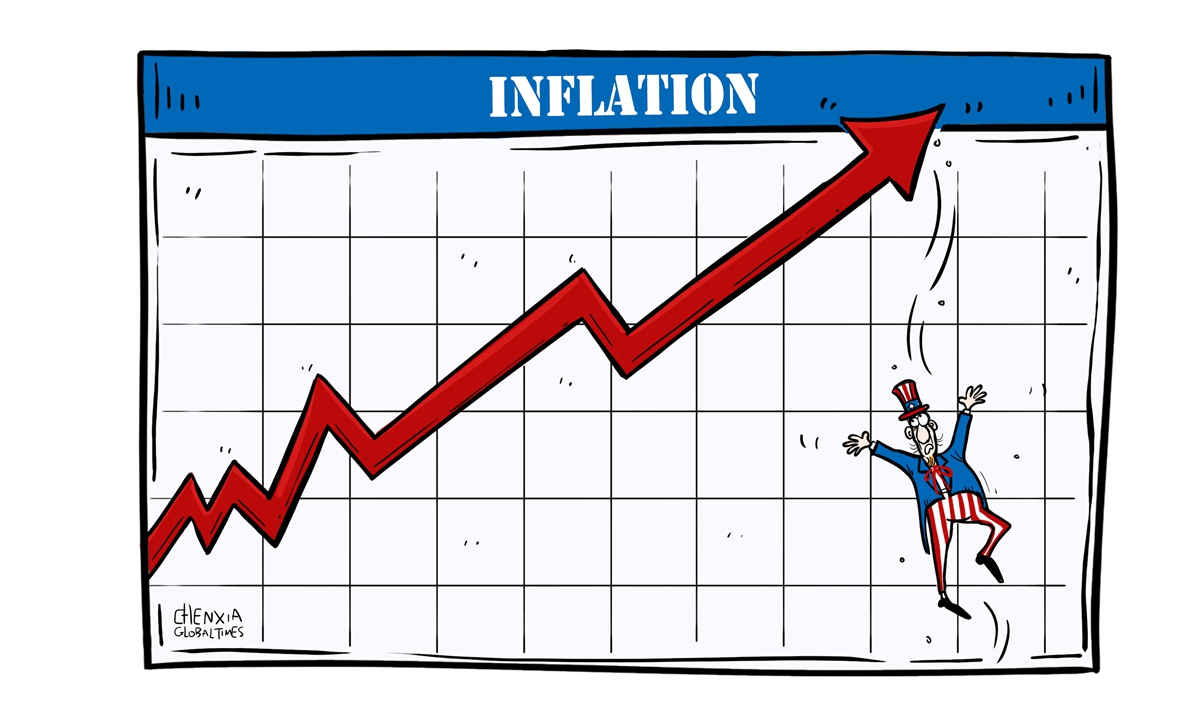

At present, inflation in the West, particularly in the US, has slowed in recent months as a result of the Federal Reserve's aggressive monetary tightening, but consumer prices remain stubbornly high and it is hard to tell whether a slowing rate hike pace could continue to bring inflation down.

The reasons behind the high inflation are complex, but if someone took time to dig the root cause, it is because of the US' blind and unlimited money printing aimed at maintaining "prosperity" in previous years. In addition, the US disruption of the global industrial chain, the Russia-Ukraine conflict and other factors have all contributed to the rise in supply chain costs.

China has never been and will not be a source of global inflation. When it comes to issuing stimulus measures, China still has plenty of options and will not adopt reckless stimulus policies. According to Goldman Sachs, China's inflation will not rise as much as in Western countries next year, with core CPI inflation increasing from 0.7 percent in 2022 to only 1.2 percent in 2023, media reports said.

At this juncture, any attempt to play up China's "impact" on global inflation could only be indicative the Western uncertainty about tackling the problem. But shirking the pressure to others is not the solution. In the face of the inflation challenge, the world's major economies, especially those in the West, should put more emphasis on addressing their own issues with determination and courage, instead of dodging the problems.

RELATED ARTICLES