Wind turbines and solar panels work together on the heights of Bajie Mountain in Yangshan, South China's Guangdong Province, on April 19, 2026. Photo VCG

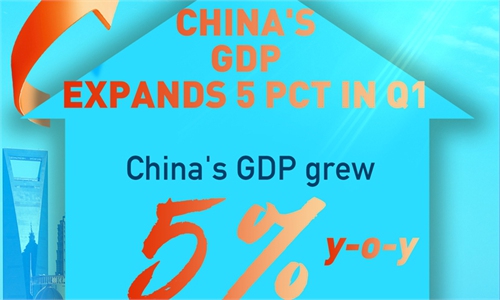

China’s GDP grew 5 percent in the first quarter. In terms of macroeconomic growth, the economy accelerated in the first three months on both a year-on-year and quarter-on-quarter basis, and the figures exceeded expectations.

The acceleration of growth pace was achieved on the back of a relatively high base last year, which was 5.4 percent. And, it is noteworthy that first-quarter growth is positioned in the upper range of China’s GDP growth target of 4.5 to 5 percent. This is why we describe the figure as indicating that China’s economy has gotten off to a strong start and shows resilience.

It is believed that, given the stronger-than-expected GDP growth in the first quarter, this has created favorable conditions for achieving the full-year GDP growth target. There remains a good chance for GDP to stay within the 4.5 to 5 percent range in the coming quarters.

The base effect is also supportive, as last year’s GDP growth was high at the beginning and gradually tailed off. However, if the Middle East conflict does not end soon, the quarter-on-quarter GDP growth could possibly ease in the next few quarters, as foreign demand matters to the Chinese economy.

In breakdown, China’s total retail sales of consumer goods expanded by 2.4 percent year-on-year in the January-March period, while fixed-asset investment jumped by 1.7 percent year-on-year. A close look at the figure shows that the situation of strong supply and weak demand has been improved to some extent, and the contribution of domestic demand has increased.

Regarding boosting consumption, the first priority is to stimulate domestic demand. Revitalizing domestic demand has two components: boosting investment and boosting consumption. While consumption usually receives more attention, the role of investment this year should not be underestimated. This is the first year of China’s 15th Five-Year Plan (2026-30) period, and we have already seen a notable rebound in investment growth in the first quarter.

When it comes to consumption, more efforts should be made to shift from short-term policy incentives to more medium- and long-term measures. These aim to enhance households’ consumption capacity and increase their willingness to consume. In addition, from the perspective of consumption scenarios, the country should encourage people to derive greater satisfaction from consumption, rather than relying solely on short-term stimulus.

For example, more consumption scenarios could be created – through infrastructure and other measures – to unlock consumption potential. This includes initiatives such as the Jiangsu Football City League, as well as tourism, concerts, and other emerging forms of entertainment consumption.

There remains considerable unmet demand, much of which is concentrated in the services sector rather than in physical goods. As a result, service consumption is becoming an increasingly important focus for the country. Recently, the State Council, China’s cabinet, issued a guideline on expanding capacity and improving quality in the service sector, and further efforts in this area are expected this year.

Meanwhile, the consumption of services requires time and genuine experiential engagement. This is also one of the measures currently being promoted, along with boosting the income of Chinese residents.

Ding Shuang Photo: Courtesy of Ding Shuang

The internationalization of Chinese yuan is a gradual process, and there has been a growing confidence among global investors in yuan-denominated assets.

Globally, the trend toward asset diversification is clearly gaining momentum. From China’s perspective, a moderate inflation rate, coupled with rapid growth in many emerging industries, has begun lifting returns on assets, including equities. This improvement in yields, combined with global demand for safe assets, greater openness and convenience for overseas investors to invest in China’s markets, and the introduction of more hedging instruments, is expected to strengthen the appeal of yuan-denominated assets.

If this momentum continues and all beneficial factors are taken together, yuan assets could become a meaningful component of an alternative safe asset. In the coming years, Chinese yuan could play an increasingly indispensable role in global asset allocation. This also requires further efforts, including steady advancement in the internationalization of yuan, as well as higher returns on Chinese assets.

The author is the chief economist for Greater China and North Asia at Standard Chartered. bizopinion@globaltimes.com.cn

RELATED ARTICLES